[ad_1]

Eloi_Omella

Introduction

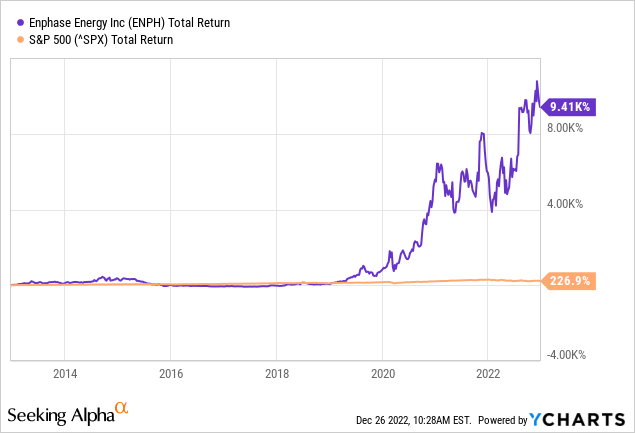

The worth of Enphase Vitality, Inc.NASDAQ:ENPH) shares have elevated in recent times. Over the previous decade, it has returned an annual 26.4%. The corporate is profitable as a result of it’s energetic within the photo voltaic business, which is a part of a clear vitality megatrend.

The corporate’s quarterly efficiency exceeded expectations. The speedy growth of the enterprise is as a result of top quality of the merchandise provided, and the superb customer support. The enterprise has been in a position to considerably lower its prices, leading to a big enhance in its gross margin. When the worth of Enphase shares fell, I added extra shares to my funding portfolio.

Firm Overview

Emphasize aggressive benefit (Enphase 3Q22 investor relations)

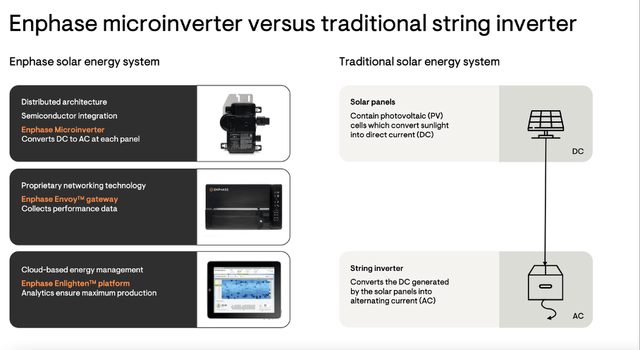

Photo voltaic microinverters, designed and manufactured by Enphase Vitality, are used to transform DC electrical energy produced by photo voltaic panels into AC electrical energy appropriate to be used in properties and companies.

Microinverters from Enphase are suitable with a variety of photo voltaic panel programs and are designed to be easy to arrange and preserve. A couple of hundred nations use the corporate’s expertise in photo voltaic vitality programs for properties, companies, and utilities. Enphase gives greater than microinverters; additionally they promote battery storage programs and software program to observe and enhance vitality output and consumption patterns.

Enphase Operates In A Giant Whole Addressable Market

Enphase SAM (Enphase 3Q22 investor presentation)

The time period “serviceable addressable market” (SAM) refers back to the basic wants that may be met with the corporate’s choices. As a consequence of the truth that the whole addressable market (“TAM”) takes into consideration the demand for all photo voltaic vitality services and products, not solely these provided by Enphase, the scale of the SAM could also be smaller than in TAM.

Photo voltaic vitality system demand from residential, business, and industrial customers, in addition to demand from utilities and different massive vitality customers, are all accounted for by Enphase’s SAM. In accordance with Enphase, its SAM will attain $23 billion by 2025. In 2025, income is predicted to be $4.7B, which can put Enphase’s market share at 20%. There may be nonetheless loads of room for Enphase to develop, as the corporate is quickly increasing and gaining market share.

Enphase Is Nicely Positioned In The Trade Megatrend

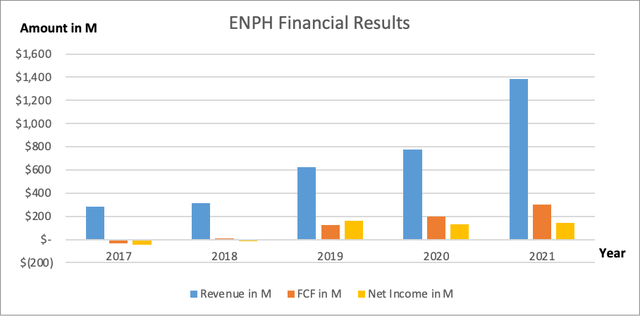

As a result of vitality transition, Enphase Vitality is ready to develop a quickly increasing market. Income has grown 48% yearly on common over the previous 4 years. Web revenue has turn out to be optimistic, and free money movement is predicted to achieve $300 million in 2021. There are robust expectations in regards to the firm’s progress: Twenty-three analysts have elevated their projections for income and earnings per share. They count on gross sales to extend yearly by 31%, reaching $3.95B by 2024. The anticipated common EPS progress from 2022 to 2024 is 25% yearly. These are bold predictions, however I’ve little doubt that Enphase will reap nice rewards from the megatrend within the photo voltaic business.

Emphasize monetary highlights (SEC and creator’s personal graphical illustration)

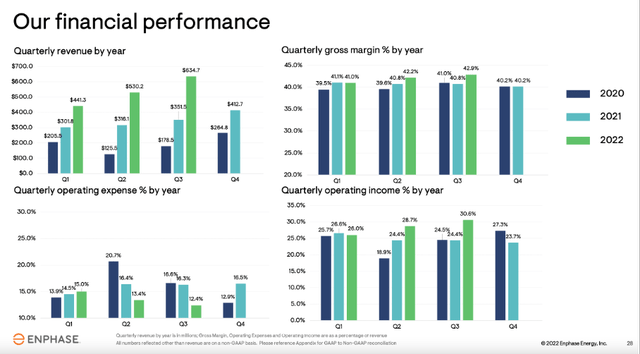

Monetary outcomes for Enphase within the third quarter of 2022 have been robust. Quarterly gross sales hit a brand new excessive of $634.7 million, up 80 p.c year-over-year. The corporate’s free money movement (“FCF”) was $179.1 million, a rise of 79% year-over-year, whereas gross margin reached 42.9%.

Monetary efficiency (Enphase 3Q22 investor presentation)

Within the third quarter, greater than 47% of all microinverter shipments have been the brand new IQ8 mannequin.

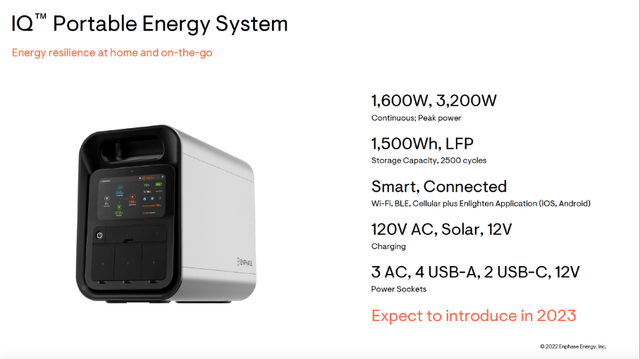

The corporate is getting ready for future success in increasing the photo voltaic vitality market. The IQ Transportable Vitality System can be added to the corporate’s choices alongside its present services and products to extend gross sales.

IQ Transportable Vitality System (Enphase’s 3Q22 investor presentation)

Enphase can be increasing its manufacturing capability to fulfill elevated demand. The present quarterly manufacturing capability of the microinverter is nearly 5 million. The primary quarter of 2023 will see microinverter manufacturing in Romania, growing the corporate’s quarterly output capability to six million microinverters worldwide.

The Inflation Discount Act (IRA) prolonged the funding tax credit score for residential photo voltaic to 30% for one more 10 years and established a standalone storage funding tax credit score with related provisions.

Though there are various issues within the chip provide chain. Do not see any points with Enphase. Enhancements are made to the distribution of particular person parts. CEO Badri Kothandaraman is optimistic:

There are nonetheless some tight spots that come up now and again and our operations staff does an incredible job dealing with the scenario nicely. The logistics scenario has additionally improved barely with decreased supply instances.

The corporate’s speedy growth within the sector’s mega-trend exhibits no indicators of slowing down. The corporate’s latest restoration from the European vitality disaster attributable to the Russian fuel boycott makes the vitality transition an much more pressing situation. I imagine that because of its glorious market place, Enphase will proceed to develop quickly within the coming years.

Shares are costly

Whereas the corporate’s progress prospects are vibrant, buyers must also think about the present share value.

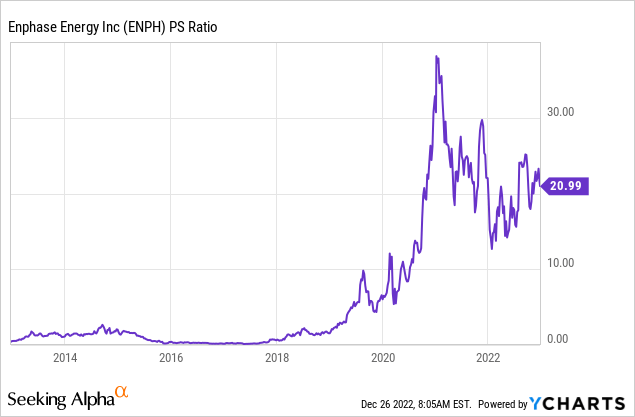

For a progress firm, I often want the worth to gross sales ratio. With rising gross margins, as within the case of Enphase, this ratio is undesirable. Gross margin was 42% (GAAP), up from 20% in 2017.

Over time, the corporate has grown tremendously. With a Worth To Gross sales ratio of 21, the corporate is very valued. The P/S ratio is rising at an alarming charge, because the chart exhibits.

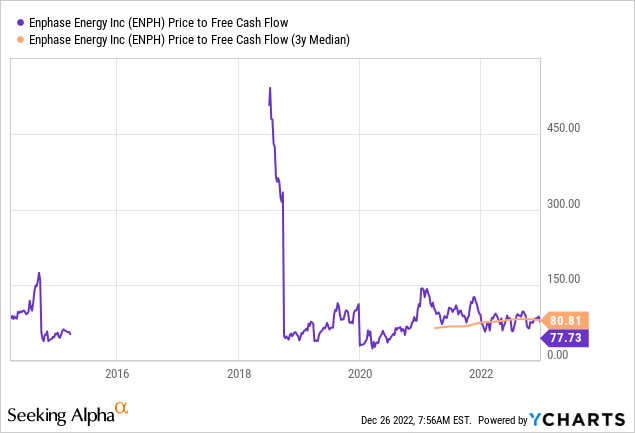

On account of the regular progress of the gross margin, a comparatively excessive P/S ratio is predicted. The P/FCF (free money movement) ratio seems to be the best choice for gaining perception into the corporate’s valuation. As seen within the graph under, the present P/FCF ratio of 78 is decrease than the three-year common of 81.

With a 53% enhance year-on-year from 2021, free money movement exhibits continued speedy growth. On the present inventory value, the worth of free money movement can be 23 by the top of 2025 if this speedy growth is maintained over the following three years. Contemplating that the Federal Reserve has been elevating rates of interest to forestall extreme inflation, I feel the corporate’s present valuation is a bit costly.

Conclusion

Photo voltaic microinverters are used to transform DC electrical energy generated by photo voltaic panels into AC electrical energy appropriate to be used in properties and companies. A couple of hundred nations use the corporate’s expertise in photo voltaic vitality programs for properties, companies, and utilities. Enphase is increasing quickly and gaining market share rapidly. Income has grown 48% yearly on common over the previous 4 years.

Introduced by Enphase Vitality, Inc. robust quarterly outcomes as gross sales elevated 80% yr over yr. Analysts count on gross sales to extend yearly by 31%, reaching $3.95B by 2024.

The speedy growth of Enphase Vitality, Inc. the photo voltaic mega-trend exhibits no indicators of slowing down. Prices decreased and gross margin elevated to 42%, from 20% in 2017. With a 53% year-on-year enhance from 2021, free money movement exhibits continued speedy growth. The inventory valuation of Enphase Vitality, Inc. an essential a part of funding choice making. I feel the present valuation of the corporate is kind of costly. When the worth of Enphase shares fell, I added extra shares to my funding portfolio.

[ad_2]

{kind=link}